The insurances industry is concerned about a type of policy that has just skyrocketed in cost across the United States. In fact, several companies have begun to warn their clients of increases for the next renewal. What has happened? The problem is coming from outside our planet, or rather, from the atmosphere, and it is getting worse and worse.

These insurances are raising concerns: attention to the cost in all U. S.

Home insurance is costing more, and more across the USA, and the primary factor in this being climate change. For instance, global warming as a consequence causes greater intensity and frequency of extreme weather events such as hurricanes, floods, and wildfires.

This greater risk calls right into the account of what the homeowners pay for it. Higher loss ratios have caused premiums to increase dramatically next to those bearing the brunt of the disaster costs. Homeowners do some excessive and insufficient to control risks which climate danger poses in the same time.

On the contrary, many of them are facing the options as insurance rates are overshooting incomes. This making trend really shows us where the climate change goes to – physical property, security of income at the same time. Infrastructure can be adjusted to withstand growing insurance losses.

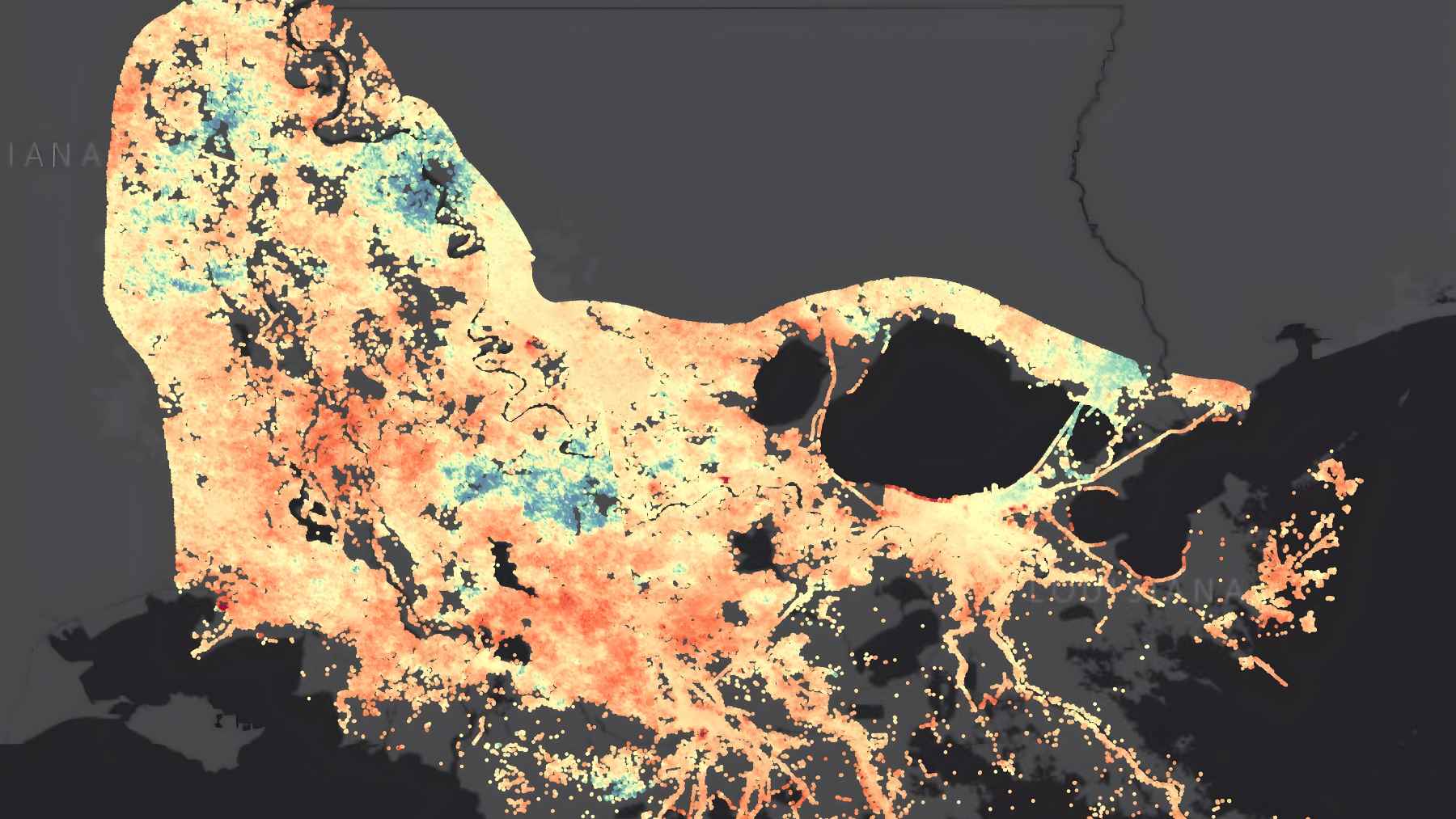

Insurers look at a home’s proximity to the coast as a major risk factor. Homes farther inland may see smaller increases, but hurricane winds can still cause roof and siding damage deep into the interior of coastal states. With hurricane season extending later into the year, even homes far from the coast could see insurance costs rise.

Home insurances are skyrocketing: there´s no good news for this year

Insurance firms nowadays reward policyholders who actively implement measures to avoid or reduce the negative effects of climate change, like damages to the home, etc. Such measures include the likes of putting in place hurricane clips or lifting up air conditioning units to levels above the flooding area.

Providers include in their plans discounts and maybe getting the whole property inspected to find out what needs to be done to comply with state and local building and safety standards. A rebate applies after the fourth inspection.

Implementation of these preventive measures as a result may lead to come aware discounts from 5% through 40%. This rule applies to very high risk residents as well as those in moderate-risk zones for whom these mitigation discounts could mean the difference between being able to afford or not the ongoing coverage.

The problem is getting worse: climate change is the main reason for concern

Many homeowners are struggling to afford rising insurance costs caused by climate change risks. Some are seeing their annual premiums double or even triple in price. This pricing surge is pushing insurance coverage out of reach for a growing number of households.

Those with fixed or lower incomes are being hit the hardest. These homeowners are faced with impossible choices – pay the steep premium hikes or lose their insurance. Dropping coverage could leave them totally exposed in the event of a loss.

Unfortunately, some homeowners who can still barely afford higher premiums are seeing their policies dropped or non-renewed by insurers anyway. Carriers are retreating from areas deemed too risky, creating insurance deserts. This forces people to turn to state insurance plans, which are limited and more expensive.

Without insurance, recovering from a disaster becomes nearly impossible. Uninsured losses can bankrupt families and jeopardize their financial security. More must be done to ensure affordable coverage and housing stability as climate risks escalate.

As you can see, the impact of climate change on home insurances is not minor, but as worrying as the impact it will have on life insurance when deaths due to heat waves double. These predictions have been confirmed over the last few years, and paint a scenario for insurers that will be similar to that of the pandemic. However, in this case, it will have a greater impact than ever before.